|

Investigating the Drivers of Mobile Banking Service Adoption in Khulna City

Md. Mehedi Hasan1*,Rifa Tamanna1 and Md. Nahid Hasan1

1Economics Discipline, Social Science School, Khulna University, Khulna 9208, Bangladesh |

|

Keywords |

|

Abstract |

|

Mobile Banking, Adoption, Ease of Use, Infrastructural Facilities, Perceived Trust, Perceived Risk, Peer Influence |

|

The primary focus of this paper is to identify the key factors that influence the adoption of mobile banking services in Khulna city, Bangladesh. Based on a structured questionnaire survey of 200 respondents selected through multistage sampling, this research examines how demographic, socio-economic, and perceptual factors affect users’ behavior toward mobile banking. The study employs descriptive statistics, principal component analysis (PCA), and binary logistic regression to determine that age, gender, expenditure, and savings are significant socio-economic indicators of adoption. Results show that adoption rates are higher among younger individuals, males, and those with greater savings and expenditures. Among the main factors, ease of use and perceived trust have a positive influence on adoption, while perceived risk has a negative impact, and both are statistically significant. Peer influence and infrastructural facilities are not statistically significant. Although infrastructural facilities have a positive relationship with mobile banking adoption, peer influence shows a negative relationship. This study recommends developing mobile banking strategies tailored to older populations, with an emphasis on simpler interfaces and increased awareness. These recommendations offer valuable insights for policymakers and financial service providers aiming to enhance financial inclusion and strengthen banking strategies in both rural and urban areas of Bangladesh. |

1. Introduction

Mobile Banking Services (MBS) refer to the activities and financial transactions that users can perform using smartphones or other mobile devices. Secure and convenient financial services, available at any time and from anywhere with internet connectivity, allow users to utilize MBS (Islam et al., 2017). The cause of its popularity is accessibility, security, and features centered around smartphones (Steinbock, 2005). Institutions connected to finance are rapidly implementing mobile banking to meet the growing demand for digital financial services and maintain competitiveness in a rapidly changing economic landscape. Particularly in third-world countries, mobile banking has become a transformative force, providing easy and smooth access to populations that were previously unbanked. Therefore, technological innovation plays an essential role in creating an inclusive and sustainable financial ecosystem (Singh and Srivastava, 2020).

Globally, MBS usage has increased significantly, with internet and mobile connectivity now reaching nearly 67% of the world's population—equivalent to approximately 5.1 billion people. Approximately 710 million new users are expected to sign up for telecom services, with a significant number located in Asia in the near future (Steinbock, 2005). Approximately 80% of households in Europe and Asia utilize mobile banking, indicating its broad appeal. However, in countries such as Bangladesh, an emerging South Asian economy with a population of approximately 164.69 million, access to formal banking services remains limited due to geographical, infrastructural, and cost-related challenges (Mamun et al., 2023). To address these issues, mobile banking has rapidly expanded and now plays a crucial role in enhancing financial inclusion.

The MBS in Bangladesh has experienced significant growth in recent years. Following the launch of mobile banking by Dutch Bangla Bank Limited on March 31, 2011, after receiving regulatory approval from the Bangladesh Bank, the industry has thrived (Hossain and Russel, 2017; Islam and Hossain, 2015; Khan et al., 2017). Leading platforms include bKash (offered by BRAC Bank) and Rocket (offered by Dutch-Bangla Bank). Furthermore, services like Nagad, MCash, SureCash, Upay, and Trust Axiata Pay (Tap) have expanded the range of available services (Mamun et al., 2023). These platforms enable users to conduct various financial activities, such as money transfers, bill payments, mobile recharges, savings, and more (Zhou, 2012; Audi, 2016). The increase in mobile internet usage in Bangladesh, combined with the widespread availability of smartphones, has further enhanced the acceptance of these services, providing added benefits, interaction, and engagement (Singh and Srivastava, 2020).

Along with growth, the acceptance rates are not equal and are influenced by various technological, demographic, and institutional factors. Concerns regarding usability and security in technology (Akhtar et al., 2020), as well as social and economic factors (such as income and education) and the level of institutional trust (Mamun et al., 2023), have a significant impact on user behavior. While prior research has primarily focused on these factors, there is a noticeable lack of comprehensive studies on how they interact in the Khulna metropolitan area, where smartphone usage is on the rise. Still, other aspects of technology adoption and usage have not been thoroughly investigated (Singh and Srivastava, 2020). The literature on self-reported bias, for example, is very lacking and has a narrow regional focus (Al Amin et al., 2022).

The objective of the study is to investigate the factors influencing the usage of mobile banking services in Khulna city. This study also examines the impact of socio-economic variables like age, income, and expenditure on usage behavior prediction. Additionally, institutions such as marketing and regulatory actions affect the accumulation of user trust. The findings of the research will play a crucial role in informing policymakers' development of policies and in shaping banks' institutions. The geographical scope within the city of Khulna may limit the level of generalizations. Any abnormality in the respondents' responses may affect the results and findings. It was challenging to use uncertain subjects because of high utilization of MBS. Lack of funds limited the scope of this research. However, this study provides valuable insights into MBS and lays the groundwork for future research.

2. Literature Review

2.1 Factors Influencing the Adoption of MBS in Bangladesh

Mobile banking is making rapid progress in Bangladesh, with banks increasingly investing in this sector (Lee et al., 2021). Trust, relative advantage, and perceived risk are the salient influencing factors that ensure mobile banking acceptance. While perceived risk is an important issue, the relative advantage has a significant positive impact. Mobile banking customers believe it saves time and money. These findings can reflect cultural and economic aspects of emerging countries (Haider et al., 2018). Mobile banking is a fast and effective way to conduct transactions. It provides 24-hour access, eliminates the need for travel, and has nearby agent sites for accessibility (Khan et al., 2017). Five key factors —risk, accessibility, comparative advantage, cost, and simplicity —ensure the adoption of mobile banking. The study found that increased costs reduced adoption rates. People consider risk as the pivotal factor that affects the adoption of mobile banking in Bangladesh. The study provides valuable insights into users' perspectives and the technical aspects of the MBS (Mamun and Rana, 2023). Mobile banking is gaining popularity in Bangladesh as financial institutions transform the industry (Lee et al., 2021). The platform is being updated to provide highly interactive mobile applications that meet customers' needs.

Financial institutions have introduced mobile banking to attract customers and provide convenient financial solutions (Akhter et al., 2020). Perceived usefulness, security, and technology competency influence customers' influence towards mobile banking, which is found to be positive. To remain competitive, service providers utilized some minor variables, such as trust, usability, and privacy. Understanding the factors that influence customer adoption of mobile banking will help financial institutions formulate their goals (Akhter et al., 2020). M-banking offers individual customers daily banking services and quick access to banking information (Lee et al., 2021). The adoption of mobile banking in India has not seen significant growth, despite the rapid expansion of information technology and mobile banking services. Perceived usefulness, ease of use, risk, and trust are substantial factors in m-banking adoption, while perceived cost is not a significant barrier. Trust and risk are significant determinants of m-banking adoption, indicating potential market growth for online banking services (Sharma et al., 2017).

Mobile banking enables customers of mobile financial institutions to make deposits, withdraw, and send/receive funds via a mobile device like a phone or digital assistant (Haider et al., 2018). The study examines the factors influencing consumer acceptance of mobile banking in Bangladesh, revealing that four key factors significantly impact attitudes towards mobile banking: infrastructure, self-control, social influence, and perceived risk. The other four factors, ease of use, need for interaction, perceived usefulness, and customer service, have less significant levels. Perceived usefulness (PU), self-control (SC), infrastructure facilities (IF), and need for interaction (NFI) affect MBS adoption, but ease of use is the most critical factor. To enhance ease of use, Microfinance Institutions (MFIs) should focus on features like easy account opening process, rapid money transfer, increasing ATM booths, and access everywhere (Islam et al., 2017)

2.2 Age Influence

Older people are using MBS less than younger generations (Lee et al., 2021). Younger generations are known as tech natives due to their high engagement with technology and their curiosity about the unknown. Because of its sophisticated nature, reliability, speed, and efficiency, young generations use it often for various perspectives (Khan et al., 2017).

On the other hand, older people in Bangladesh sometimes express a more arrogant attitude towards mobile banking usage (Suh and Han, 2002). Due to a lack of technical knowledge, limited access, and some privacy issues, older people often feel afraid to use MBS. Due to trust issues and concerns about using digital platforms, older people tend to rely more on conventional banking than on digital services (Elhajjar and Ouaida, 2020).

2.3 Gender Influence

The role of Gender in mobile banking seems impractical, but it has shown a significant effect on MBS adoption. MBS are further influenced by socio-economic and demographic aspects (Islam, 2015). Men are more likely to adopt mobile banking due to having proper access to technology, being financially literate, and conforming to social norms. Men tend to have more autonomy in making financial decisions and accessing digital services, which is likely to lead to subsequent technology adoption (Suh and Han, 2002). Women usually do not own a mobile phone in Bangladesh and face some barriers (lack of knowledge, not enough confidence, etc.) that hinder their usage of MBS (Haider et al., 2018). Moreover, women in this country often follow cultural norms that limit their engagement in financial transactions and decision-making (Islam, 2015).

2.4 Educational Qualification Influence

In Bangladesh, the length of schooling has a significant influence on the adoption of mobile banking. Education can ameliorate the ability to understand the process of using MBS properly (Akhter et al., 2020). Those with educated backgrounds are familiar with the safety mechanisms and user-friendly features of MBS. This digital literacy makes them more likely to adopt mobile banking over traditional systems (Akhter et al., 2022). Low literacy levels stop people from understanding banking terms and concepts, creating barriers to trust and use. Literacy level has a significant influence on increasing awareness and reliability in both urban and rural areas (Kabir, 2013).

2.5 Occupational Status Influence

When discussing mobile banking in Bangladesh, it is undeniable that occupation plays a crucial role in the decision to adopt MBS. Self-employed individuals or those working in the informal sector often face challenges, including low literacy and skepticism regarding the privacy of MBS (Islam, 2015). Day laborers and farmers involved in agricultural production are less likely to use MBS due to their asymmetrical income streams (Khan et al., 2017). Furthermore, institutional support, including banking awareness programs offered by employers, has been shown to increase mobile banking usage among formal employees (Akhter et al., 2020).

2.6 Income and Expenditure Influence

Income level is one of the most important factors influencing the adoption of mobile banking in Bangladesh. People with limited income often live on a small income, which restricts their ability to use (Haider et al., 2018). The expenses associated with mobile banking, including data charges and transaction fees, can deter this demographic from utilizing these services. Furthermore, those who live hand-to-mouth do not get enough time to think about technology. This hinders their interest and capacity to participate in mobile banking systems. In contrast, higher expenditure individuals are used to using MBS even in day-to-day transactions (Sharma et al., 2017). Higher-income individuals typically use mobile phones and have access to the internet, which enables them to use mobile banking.

2.7 Savings Influence

Savings play a crucial role in the adoption of MBS, particularly for individuals who seek more effective methods of securing and managing their finances (Hossain and Hossain, 2015). The convenience of establishing savings accounts via mobile banking has fostered adoption, particularly among students and low-income populations. For instance, digital wallets and mobile banking applications enable users to automate their savings or pursue micro-savings goals without the need to visit banking establishments physically. This feature is especially attractive to younger individuals (Hossain and Hossain, 2015). Additionally, mobile banking mitigates issues related to traditional savings methods, such as elevated transaction fees and limited access in rural regions. The extensive use of mobile phones, coupled with the increasing availability of mobile financial services (MFS) in rural Bangladesh, has successfully broadened access to savings options. Mobile banking applications offer enhanced transparency and improved monitoring of savings, thereby promoting financial discipline among users (Suh and Han, 2002).

2.8 Ease of Use Influence

MBSs in Bangladesh, such as Bkash and Nagad, have increasingly emphasized usability by incorporating QR codes, biometric logins, and streamlined money transfer processes. These advancements are consistent with research that suggests user-friendly technology promotes wider acceptance (Khan et al., 2017). Applications for mobile banking that are intuitive and easy to navigate, along with providing seamless access, are more likely to attract and retain customers (Jadil et al., 2021). The simplicity of the interface, speed of transactions, and availability of essential services such as balance inquiries, fund transfers, and bill payments all contribute to enhancing the overall user experience (Akhter et al., 2020). Therefore, improving ease of use remains a fundamental aspect in encouraging mobile banking adoption, especially among the younger, tech-savvy student demographic, who constitute a significant segment of the unbanked population in Bangladesh.

2.9 Infrastructural Facilities Influence

Infrastructure facilities play a pivotal role in the acceptance and success of mobile banking. The availability and quality of these facilities significantly influence customers' willingness and ability to engage with MBS (Hossain and Hossain, 2015). Key infrastructure components include internet access, mobile network coverage, the availability of mobile devices, and the stability of financial technology platforms. High-quality internet access is essential for the seamless operation of mobile banking applications (Haider et al., 2018). As noted by Chawla and Joshi (2017), regions with superior internet connectivity exhibit higher rates of mobile banking adoption due to reliable and swift access to financial services. Conversely, inadequate internet connectivity can lead to frequent disruptions and delayed transactions, thereby discouraging users from utilizing MBS. Mobile network coverage constitutes an essential factor (Hossain and Hossain, 2015). Sufficient coverage ensures that MBS remains accessible at all times and from any location. Users encounter considerable challenges when attempting to utilize these services in areas characterized by insufficient network coverage. The adoption rates of mobile banking are notably higher in regions where there is a greater prevalence of mobile devices. Therefore, addressing infrastructural deficiencies is imperative for the extensive and equitable implementation of MBS (Makanyeza, 2017).

2.10 Perceived Trust Influence

The significance of perceived trust is paramount in the adoption of mobile banking, functioning as a foundational element in consumers' decision-making processes (Hossain and Hossain, 2015). In examining the factors that influence mobile banking adoption, trust is revealed as a multidimensional construct, encompassing attributes such as reliability, security, privacy, and competence. Perceived trust plays a crucial role in mitigating perceived risk and facilitating users' acceptance of mobile banking technology (Kabir, 2013). Moreover, it highlights the dynamic nature of trust in the realm of mobile banking, suggesting that trust extends beyond initial impressions and evolves progressively through ongoing interactions and experiences. These findings highlight the crucial role of perceived trust in the adoption of mobile banking (Mamun and Rana, 2023).

2.11 Perceived Risk Influence

Perceived risk is a crucial element that affects the acceptance of MBS. It encompasses various dimensions, including financial risk, security risk, privacy risk, and performance risk, all of which significantly influence users' decision-making processes. Financial risk pertains to the possibility of financial loss resulting from transaction errors, as noted by Uddin and Begum (2023). Concerns about financial risks can deter users from using mobile banking, stemming from fears of unauthorized access to their accounts and breaches of sensitive financial data. Security and privacy risks are especially relevant in the realm of mobile banking, as highlighted by Kabir and Sultana (2021). Moreover, research indicates that risk goes beyond mere advisories, contributing to the development of confidence in engaging with new technologies. When individuals observe their friends or classmates employing mobile banking applications, they are more inclined to regard these platforms as dependable and user-friendly (Islam et al., 2017). The associated risks include the potential for personal information to be disclosed to unauthorized individuals and the risk of identity theft (Makanyeza, 2017). Privacy issues, such as the unauthorized usage of personal information by third parties, may significantly erode trust in MBS, thereby hindering their adoption (Ahmed and Hossain, 2022). Ultimately, the perception of risk affects the utilization of MBS in numerous ways. Mitigating these concerns through enhanced security protocols, robust privacy policies, and consistent application performance can significantly influence customers' readiness to adopt mobile banking technologies.

2.12 Peer Influence

Peer recommendations are an essential source of information regarding MBS. Positive endorsements from peers who have successfully embraced mobile banking can alleviate perceived risks and foster trust among prospective users (Haider et al., 2018). This is particularly significant in the context of Bangladesh, where trust issues related to technology and financial institutions frequently present challenges to adoption (Suh and Han, 2002). Peer influence refers to the impact that friends, family, and colleagues exert on individuals’ choices. The attitudes and behaviors of individuals are often influenced by the opinions and actions of those around them. In the case of mobile banking, many individuals rely on the advice and experiences shared by their peers before deciding to use the service (Kabir, 2013). Moreover, the influence of peers goes beyond simple endorsements, contributing to a sense of assurance in engaging with new technologies. When individuals observe their peers or classmates using mobile banking applications, they are more likely to use these platforms as dependable and easy to use (Islam et al., 2017).

2.13 Research gap

Globally, numerous studies have examined the factors influencing the adoption of mobile banking services. However, from the Bangladeshi perspective, such works are limited in number. Most global and national studies highlight factors such as perceived risk, trust, benefits, costs, and security. Some Bangladeshi studies include demographic and socio-economic factors like age, Gender, education, income, expenditure, and savings. In this paper, we aim to assess the impact of mobile banking facilities (including ease of use, perceived trust and risk, and peer influence) on mobile banking service adoption, alongside socio-economic and demographic variables.

3. Methodology

3.1 Study Area Selection

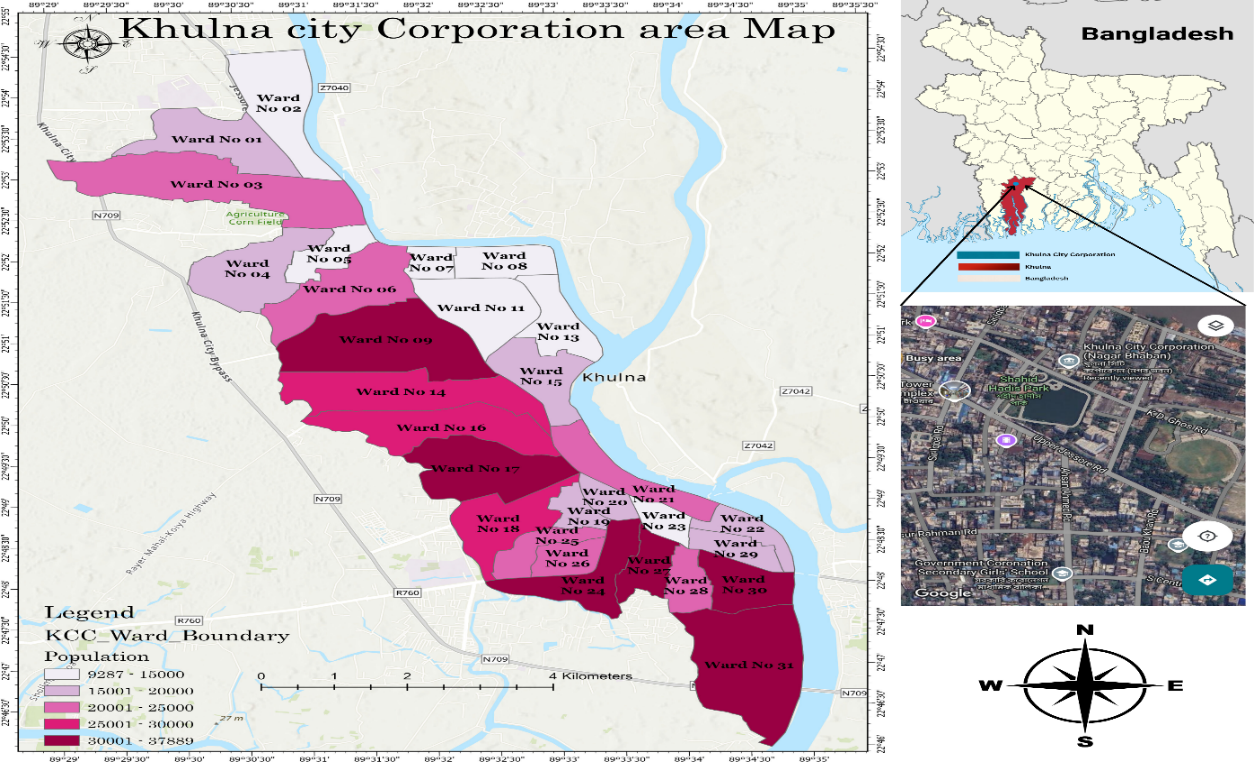

Mobile banking is gaining popularity everywhere in Bangladesh, particularly in Khulna city. For this reason, the authors planned to evaluate these pressing issues more thoroughly. As we know, there are twelve city corporations across the country, and we have chosen the Khulna City Corporation (KCC) as our study area conveniently. Subsequently, the authors selected five wards randomly out of 31 administrative wards of KCC utilizing a simple random sampling method, specifically Ward No. 06 (Daulatpur), Ward No. 14 (Boyra), Ward No. 17 (Sonadanga R/A), Ward No. 24 (Nirala R/A), and Ward No. 28 (Tutpara).

Figure 1: Khulna City Corporation

Source: Field Survey, 2024

3.2 Sampling Technique

To fulfill the study's objective and answer the research questions, the authors collected data solely from primary sources. This study employed a multistage sampling technique for data collection. For broader area selection, we employed non-random sampling, specifically convenience sampling. During the process of specific ward selection, we applied simple random sampling from the list of city corporation wards. In the initial stage, we selected KCC as one of the 12 city corporations. Finally, the study employed systematic random sampling within each selected ward to identify respondents. Data collection in the organized residential areas of Ward No. 14 (Boyra), Ward No. 17 (Sonadanga R/A), and Ward No. 24 (Nirala R/A) was conducted by selecting every fifth household, commencing from a randomly selected point within each neighborhood.

In contrast, due to the lack of planned residential zones in Ward No. 06 (Daulatpur) and Ward No. 28 (Tutpara), data collection began from the main road of each ward, with every third household being selected along accessible streets. This methodology ensured both consistency and spatial diversity in the selection of respondents. After all, we surveyed 200 mobile phone users, with 40 participants from each ward.

3.3 Variable Identification

In this section, dependent and explanatory variables are represented by a table. The list of variables that are used in this study is given in Table No. 1 as follows:

Table 1: Variables Identification of the Study

| Category of Variables | Variable Name / Explanatory Variables | Unit of Measurement / Dependent Variables | Literature |

|---|---|---|---|

| Adoption of Mobile Banking Service Account | Dummy (Yes=1, No=0) | Mamun et al., 2023 | |

| Personal Information | Age | Years | Akhter et al., 20201 |

| Gender | Male = 1, Female = 0 | Suh and Han, 2002 | |

| Educational Qualification | Year of Schooling | Kabir, 2013 | |

| Marital Status | Married=1, Unmarried=0 | Suh and Han, 2002 | |

| Religion | Hindu=1, Muslim=0 | Akhter et al., 20201 | |

| Occupational Status | Housewife=1, Otherwise=0 | Field survey, 2024 | |

| Living Arrangement | Own House =1, Rent house=0 | Suh and Han, 2002 | |

| Family Type | Joint =1, Nuclear =0 | Kabir, 2013 | |

| Household Size | In Number | Hossain and Hossain, 2015 | |

| Earning Member of Family | In Number | Kabir, 2013 | |

| Socio-economic status | Household Income | BDT/ Month | Suh and Han, 2002 |

| Household Expenditure | BDT/ Month | Hossain and Hossain, 2015 | |

| Household Savings | BDT/ Month | Kabir, 2013 | |

| Respondent Income | BDT/ Month | Suh and Han, 2002 | |

| Respondent Expenditure | BDT/ Month | Hossain and Hossain, 2015 | |

| Respondent Savings | BDT/ Month | Kabir, 2013 | |

| Any Time Transaction | Likert-Scale | Akhter et al., 2020 | |

| Fast Money Transfer Advantage | Likert-Scale | Jadil et al., 2021 | |

| Ease of Use (EU) | Saves Consumers Time | Likert-Scale | Mamun et al., 2023 |

| Can be used without a Bank | Likert-Scale | Mamun et al., 2023 | |

| Easy to Open an Account | Likert-Scale | Akhter et al., 2020 | |

| Available customer Agent | Likert-Scale | Makanyeza, 2017 | |

| Smooth Account Management System | Likert-Scale | Chawla and Joshi, 2017 | |

| Infrastructural Facilities (IF) | Network Condition | Likert-Scale | Mamun et al., 2023 |

| Available Service | Likert-Scale | Makanyeza, 2017 | |

| Better Service than Traditional Banks | Likert-Scale | Chawla and Joshi, 2017 | |

| Customer Agents' Ability | Likert-Scale | Mamun and Rana, 2023 | |

| Perceived Trust (PT) | Customer Agent Protects the Confidentiality | Likert-Scale | Kabir, 2013 |

| Customer Service Support | Likert-Scale | Mamun and Rana, 2023 | |

| Friends Influence | Likert-Scale | Islam et al., 2017 | |

| Family Influence | Likert-Scale | Suh and Han, 2002 | |

| Peer Influence (PI) | Many people use | Likert-Scale | Islam et al., 2017 |

| Customer Agent Influence | Likert-Scale | Suh and Han, 2002 | |

| Professional Purpose Influence | Likert-Scale | Islam et al., 2017 | |

| Due to a transaction error, there might be a loss of money | Likert-Scale | Ahmed and Hossain, 2022 | |

| Biometrics privacy | Likert-Scale | Field survey, 2024 | |

| Perceived Risk (PR) | Personal privacy at risk | Likert-Scale | Haider et al., 2018 |

| Provide a successful Payment process without risk | Likert-Scale | Ahmed and Hossain, 2022 | |

| Hacker risk | Likert-Scale | Haider et al., 2018 |

Source: Field survey, 2024

**Likert Scale has been measured as 1 to 5 point scale (Strongly Agree=5, Agree=4, Neutral =3, Disagree=2, Strongly disagree=1).

3.4 Econometric Analysis

Primarily, this study employed a quantitative, cross-sectional analysis. To fulfill the objective of this study and answer the research question, data were analyzed using statistical and econometric tools. Research used STATA and MS Excel as statistical packages to run statistical analysis in the study. Descriptive statistical tools, such as pie charts, bar charts, and tables, are used in analysis. For inferential purposes, probabilistic tools such as the logistic regression model and Principal Component Analysis (PCA) have been incorporated.

3.4.1 Analytical Tools

The research questions aim to identify the primary factors influencing respondents' adoption of mobile banking services. Socio-economic factors and high-dimensional explanatory variables - ease of use, infrastructural facilities, perceived trust, perceived risk, and peer influence. Under high-dimensional explanatory variables, there are 24 components. We used Principal Component Analysis (PCA) to reduce dimensions (variables) from the high-dimensional data set of explanatory variables. The PCA process is conducted individually for each set of high-dimensional explanatory variables. Under high-dimensional explanatory variables, the component eigenvalue equal to or greater than one has been used to formulate the PCA index in Table No. 2. In the process of identifying key factors influencing the respondents' adoption of mobile banking services, the authors employed logistic regression analysis.

Table No. 2: PCA on the Factors Influencing Adoption of Mobile Banking Service

| Category of Variables | Components | Eigenvalue | Cumulative |

|---|---|---|---|

| Ease of Use (EU) |

Comp 1 | 1.24584 | 0.2492 |

| Comp 2 | 1.13812 | 0.4768 | |

| Comp 3 | 1.06721 | 0.6902 | |

| Comp 4 | .879897 | 0.8662 | |

| Comp 5 | .668935 | 1.0000 | |

| Infrastructural Facilities (IF) |

Comp 1 | 1.58819 | 0.2647 |

| Comp 2 | 1.20768 | 0.4660 | |

| Comp 3 | 1.01726 | 0.6355 | |

| Comp 4 | .884527 | 0.7829 | |

| Comp 5 | .768406 | 1.0000 | |

| Perceived Trust (PT) |

Comp 1 | 1.25905 | 0.4197 |

| Comp 2 | .952979 | 0.7373 | |

| Comp 3 | .787972 | 1.0000 | |

| Peer Influence (PI) |

Comp 1 | 4.18499 | 0.8370 |

| Comp 2 | .317138 | 0.9004 | |

| Comp 3 | .211516 | 0.9427 | |

| Comp 4 | .182478 | 0.9792 | |

| Comp 5 | .103877 | 1.0000 | |

| Perceived Risk (PR) |

Comp 1 | 1.52007 | 0.3040 |

| Comp 2 | 1.05182 | 0.5144 | |

| Comp 3 | .964803 | 0.7073 | |

| Comp 4 | .809881 | 0.8693 | |

| Comp 5 | .653431 | 1.0000 |

Source: Authors’ compilation based on field survey, 2024.

3.5 Econometric Model

Logistic regression is a statistical method for analyzing the likelihood of an observed class or event occurring. When there is more than one independent variable, this model was employed to calculate the marginal effect (dy/dx). In this study, the dependent variable has two possible values: 0 and 1. That is 1 for the MBS user and 0 for the non-MBS user. As a result, the outcome of factors that influence the adoption of MBS is estimated using a logistic regression model. The dependent variable is controlled by different explanatory variables (demographic characteristics, socio-economic factors, ease of use, infrastructural facility, perceived trust, perceived risk, and social influence. The general equation of this model

3.6 Limitations

The study focused on Khulna city, which may limit the applicability of the findings to other parts of Bangladesh with different socio-economic dynamics. Another limitation was that the study primarily relied on self-reported data from survey respondents. There was a possibility of response bias, where participants overstate or understate their experiences or opinions. A sample of 200 respondents is another issue for generalizing to the overall population. This might not fully capture the diverse number of experiences and factors influencing mobile banking adoption across different groups of people. The authors collected data from mobile banking service users and non-users. However, data collection from non-users of mobile banking services is a limitation, as most mobile phone users now have mobile banking service accounts. So finding a non-user is a difficult task. Despite these limitations, the authors made a concerted effort to address the research objectives fully.

4. Descriptive Analysis

In this chapter, the author analyzes the acquired data and provides an overview of the demographic and socio-economic information. Mean, median, standard deviation, minimum, maximum, etc., have been described in this part. To interpret the results, various figures and tables are used. With the help of these tools, the researcher attempts to analyze the background characteristics of the variables and evaluate the patterns of different responses from the respondents.

4.1 Demographic and Socio-economic Information of Respondents

This section of the chapter provides general information about the respondents' demographic and socio-economic status. Those are age, gender, educational qualification, income, etc.

Table No. 1: Descriptive Statistics of Respondents’ Socioeconomic Characteristics

| Variable(s) | Unit of Measurement | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Age | In year | 34.22 | 11.786 | 16 | 64 |

| Educational Qualification | Years of schooling | 11.36 | 3.48 | 3 | 17 |

| Household Size | In numbers | 4.135 | 1.074 | 2 | 7 |

| Earning Member of the Family | In numbers | 1.67 | 0.586 | 1 | 3 |

| Household Income | BDT/Month | 33,355 | 9,456.006 | 17,000 | 65,000 |

| Household Expenditure | BDT/Month | 29,530 | 7,570.048 | 15,000 | 50,000 |

| Household Monthly Savings | BDT/Month | 3,676 | 2,437.814 | 0 | 10,000 |

| Respondent Income | BDT/Month | 10,814.5 | 12,011.349 | 0 | 45,000 |

| Respondent Expenditure | BDT/Month | 5,776.5 | 1,938.864 | 3,000 | 12,000 |

| Respondent Monthly Savings | BDT/Month | 1,283.5 | 1,461.595 | 0 | 7,000 |

Source: Field Survey, 2024.

(N.B.: Obs. = Observation, Std. Dev. = Standard Deviation, Min. = Minimum & Max. = Maximum)

Table 3 presents the demographic and economic characteristics of the respondents. The minimum age of the respondents is 16 years, while the maximum age is 64 years, with an average age of 34.22 years. The maximum number of years of schooling among the respondents is 17 years, and the minimum is 3 years. In terms of family earning members, the maximum number is 3, and the minimum is 1. The respondents' household monthly income ranges from a maximum of 65,000 BDT to a minimum of 17,000 BDT. Their household monthly expenditure ranges from a maximum of 50,000 BDT to a minimum of 15,000 BDT. Household monthly savings vary between a maximum of 10,000 BDT and a minimum of 0 BDT. Regarding the respondents' individual monthly income, the maximum amount is 45,000 BDT, and the minimum is 0 BDT, with an average monthly income of 10,814.5 BDT. Their monthly expenditure ranges from a maximum of 12,000 BDT to a minimum of 3,000 BDT, with an average expenditure of 5,776.5 BDT. Finally, their monthly savings range from a maximum of 7,000 BDT to a minimum of 0 BDT, with an average savings of 1,283.5 BDT.

Table 4: Demographic Characteristics of the Respondent (Dummy Variable)

| Variable Name | Unit Of Measurement | Description | Frequency | Percentage |

|---|---|---|---|---|

| Gender | Dummy | Female = 0 | 96 | 48% |

| Male = 1 | 104 | 52% | ||

| Marital Status Dummy |

Unmarried = 0 | 52 | 27.50% | |

| Married = 1 | 145 | 72.50% | ||

| Religion Dummy |

Muslim = 0 | 123 | 61.50% | |

| Hindu = 1 | 77 | 38.50% | ||

| Occupational Status Dummy |

Others = 0 | 125 | 62.50% | |

| Housewife = 1 | 75 | 37.50% | ||

| Living Arrangement Dummy |

Rent House = 0 | 96 | 48% | |

| Own House = 1 | 104 | 52% | ||

| Family Type Dummy |

Nuclear = 0 | 143 | 71.5% | |

| Joint = 1 | 57 | 28.5% | ||

Source: Field Survey, 2024

Out of the 200 respondents, 96 are female, and 104 are male. Among them, 52 are unmarried, while 145 are married. A total of 123 respondents are Muslim, and 77 are Hindu. The respondents include 75 housewives, while the remaining 125 are engaged in various occupations, such as employment, business, education, rickshaw pulling, and day labor. In terms of housing, 104 respondents live in their own houses, while 96 reside in rented homes. Regarding family structure, 143 respondents live in nuclear families, and 57 live in joint families.

4.2 Mobile Banking Service Users’ and Non-Users’ Information

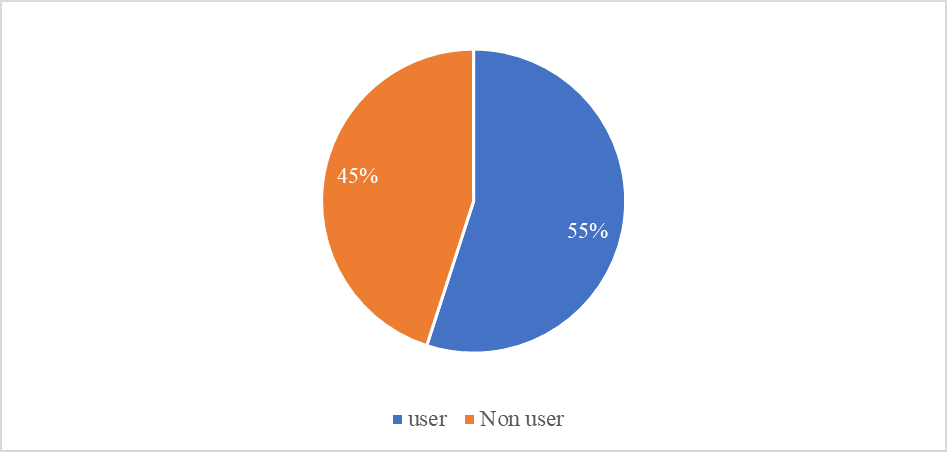

The total sample size for this study was 200. The sample is divided into two groups: users of mobile banking services and non-users. Respondents who had adopted mobile banking service accounts are categorized as the mobile banking service user group. In contrast, those who had not adopted mobile banking service accounts are categorized as the non-user group. Out of the 200 respondents, 110 had adopted mobile banking service accounts, while the remaining 90 respondents had not. The pie chart (figure 2) illustrates the percentage distribution of mobile banking service users and non-users. The mobile banking service user group constitutes 55% of the total sample, represented by the orange segment of the pie chart. In contrast, the non-user group makes up 45%, represented by the blue segment of the pie chart.

Figure 2: Mobile Banking Users and Non-Users Amount

Source: Field Survey, 2024

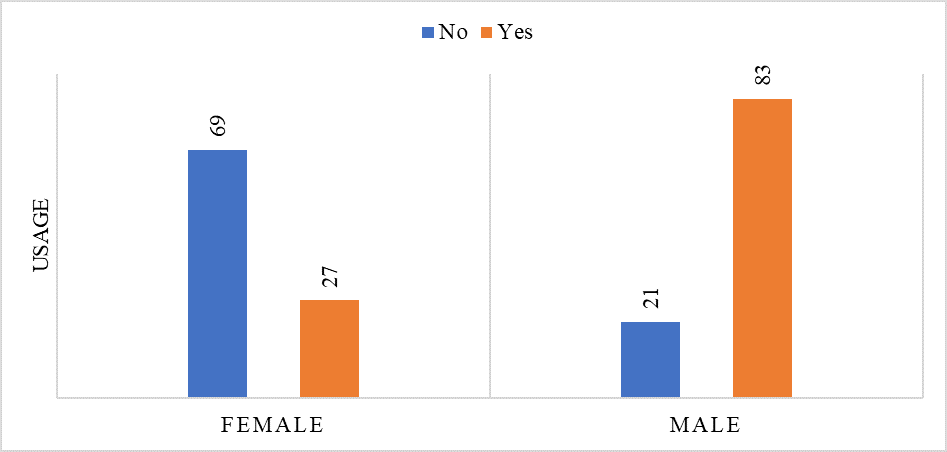

The data in Figure 3 provides insights into mobile banking usage among male and female respondents. Out of 200 participants, 110 have adopted MBS, while 90 have not. When analyzed by gender, a significant difference in usage patterns is observed.

Figure 3: Mobile Banking Users and Non-Users with respect to Gender

Source: Field Survey, 2024

Among females, 69 out of 96 have not adopted mobile banking, whereas only 27 have adopted it, indicating a lower adoption rate among female participants. Conversely, the majority of males, 83 out of 104, have adopted MBS, while only 21 have not. This indicates that male respondents are more likely to use mobile banking than female respondents.

The data illustrates the use of mobile banking within five wards of Khulna City Corporation, with a total of 200 participants—40 from each ward. Of these, 110 are users and 90 are non-users. Ward 14 reports the highest number of users at 23, while Ward 24 has the highest number of non-users at 19. Across all wards, the difference between users and non-users is quite minimal, suggesting a relatively even distribution of mobile banking adoption.

Table 5: Mobile Banking Service Users and Non-Users among Wards of KCC

| Ward Number | Mobile Banking Usage | ||

|---|---|---|---|

| No | Yes | Total | |

| No. 6 | 18 | 22 | 40 |

| No. 14 | 17 | 23 | 40 |

| No. 17 | 18 | 22 | 40 |

| No. 24 | 19 | 21 | 40 |

| No. 28 | 18 | 22 | 40 |

| Total | 90 | 110 | 200 |

Source: Field Survey, 2024

4.3 Mobile Banking Service-related Information

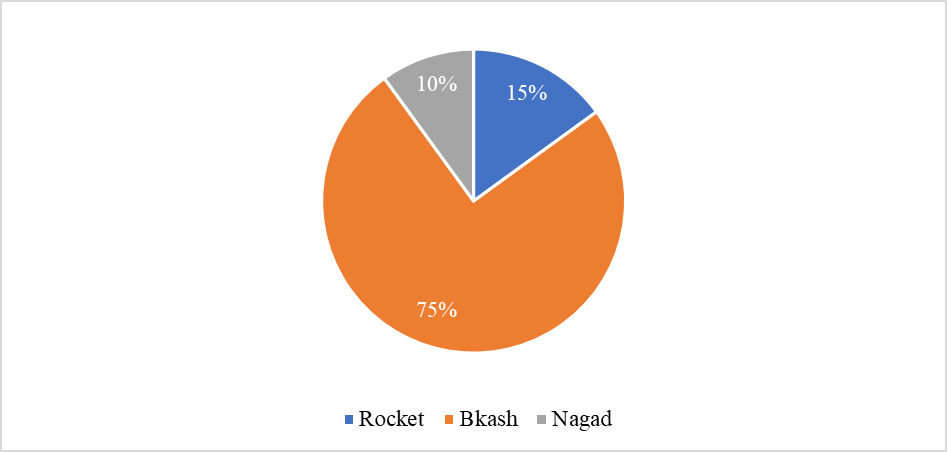

The pie chart (figure 4) illustrates the usage of different mobile banking tools among the 110 respondents who are mobile banking service users. These respondents use three types of mobile banking tools: Bkash, Rocket, and Nagad. The majority of respondents (75%) use Bkash, making it the most popular mobile banking tool.

Figure 4: Usage of Mobile Banking Tools (Users Group)

Source: Field Survey, 2024

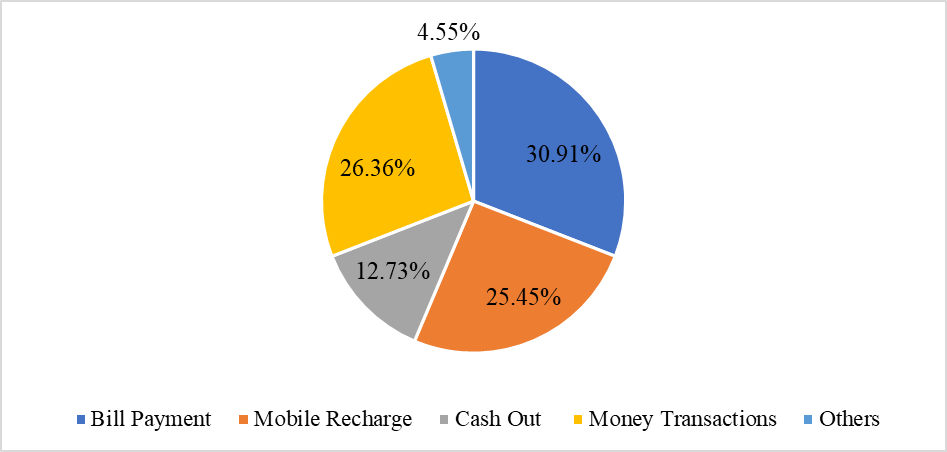

Rocket is used by 15% of respondents, while Nagad has the lowest usage, with only 10% of respondents utilizing it. This highlights Bkash as the dominant mobile banking tool among the surveyed users. The above pie chart shows which service of mobile banking accounts is used more among user groups. Mobile banking offers a range of transaction services. The service used more frequently by mobile banking service users is shown by percentage.

Figure 5: Services Used More of Mobile Banking Accounts (Users Group)

Source: Field Survey, 2024

This pie chart (Figure 5) is used to present the scenario of mobile recharge. It is 30.91% of respondents who use it for bill payment. Secondly, 26.36% of respondents use it for money transactions. Thirdly, 25.45% of respondents use it for mobile recharge. 12.73% of respondents use mobile banking accounts more for cash out. Finally, 4.54% of respondents utilize other services from their mobile banking account.

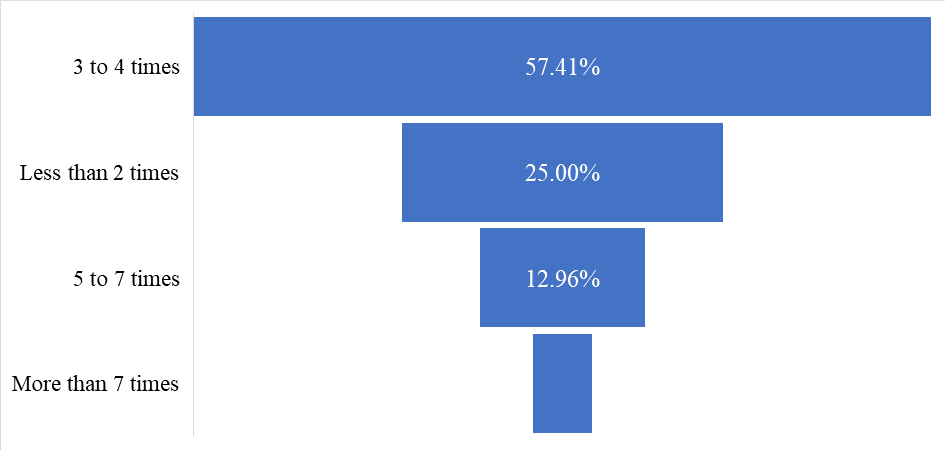

Figure 6: Usage of Mobile Banking in a Month (Users Group)

Source: Field Survey, 2024

The funnel (Figure 6) chart illustrates the frequency of mobile banking usage among respondents in a month. According to the data, the most significant proportion of respondents (57.41%) use MBS 3 to 4 times per month. Additionally, 25% of respondents use the service less than 2 times a month, while 12.96% use it 5 to 7 times. Only 4.63% of respondents use MBS more than 7 times per month. This indicates that the majority of users rely on MBS moderately, with 3 to 4 uses per month being the most common, while a small minority use the service more than 7 times per month.

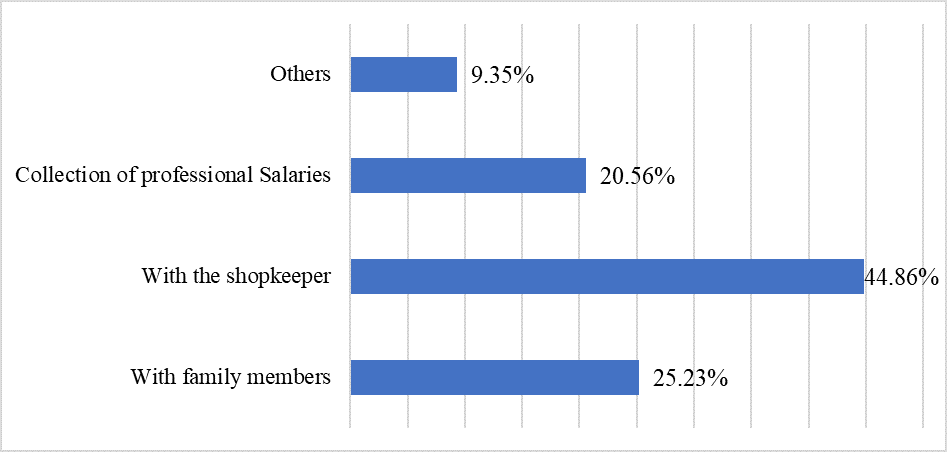

Figure 7: With Whom Mobile Banking Is Being Used (Users Group)

Source: Field Survey, 2024

This bar chart (Figure 7) shows with whom the mobile banking user group makes the most transactions. They make the most transactions with shopkeepers, which is 44.85%. Second, 25.23% of respondents make transactions with family members. Professionals use it for salary collection, 20.56% of respondents. The Other categories have the least amount, 9.34% of respondents.

4.4 Mobile Banking Service Non-User Group Information

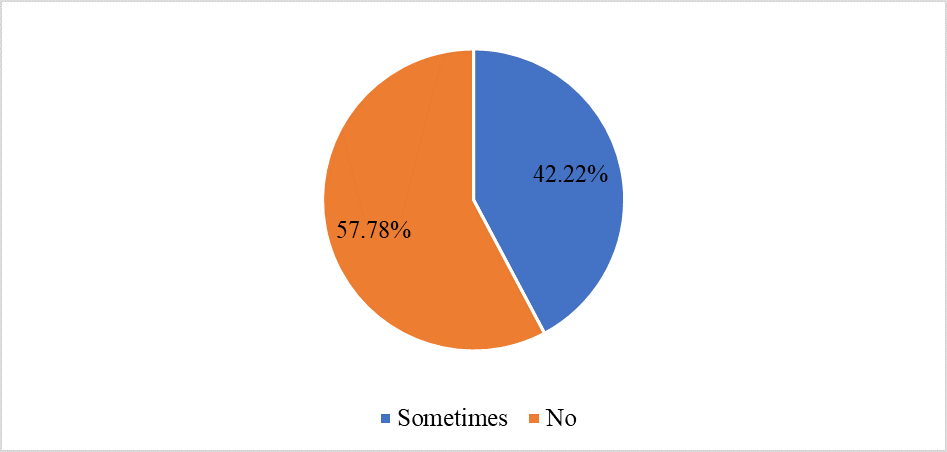

In this section, mobile banking service non-user-related information is presented with the help of bar charts and pie charts. The pie chart illustrates the need for MBS among non-user respondents, even if they do not have their own accounts. Out of 90 non-user respondents, 57.78% stated that they do not need to use MBS, while 42.22% mentioned that they occasionally need to use these services.

Figure 8: Necessity for Mobile Banking Account (Non-User)

Source: Field Survey, 2024

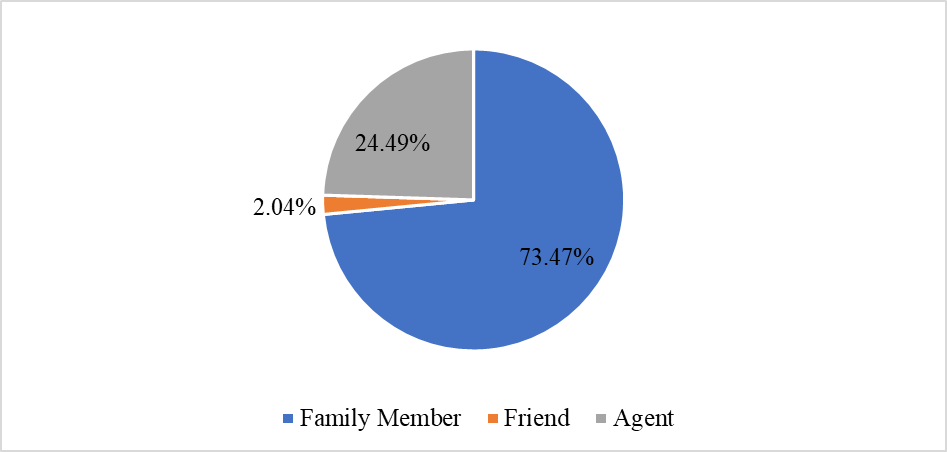

If mobile banking non-users need to use the mobile banking service occasionally, they use the account of another Mobile banking service user. Then, the account they use is represented through this pie chart

Figure 9: Whose Mobile Banking Account Use (Non-user)

Source: Field Survey, 2024

If mobile banking non-users need to use the Mobile banking service occasionally, they use the account of another mobile banking service user. Then, the account they use is represented through this pie chart. A significant majority, 73.47% of non-users, use the accounts of family members. Secondly, 24.49% of mobile banking non-users use an agent's account. Only a small fraction, 2.04%, use friends' mobile banking accounts.

Figure 10: Attitudes of Mobile Banking Non-users

Source: Field Survey, 2024

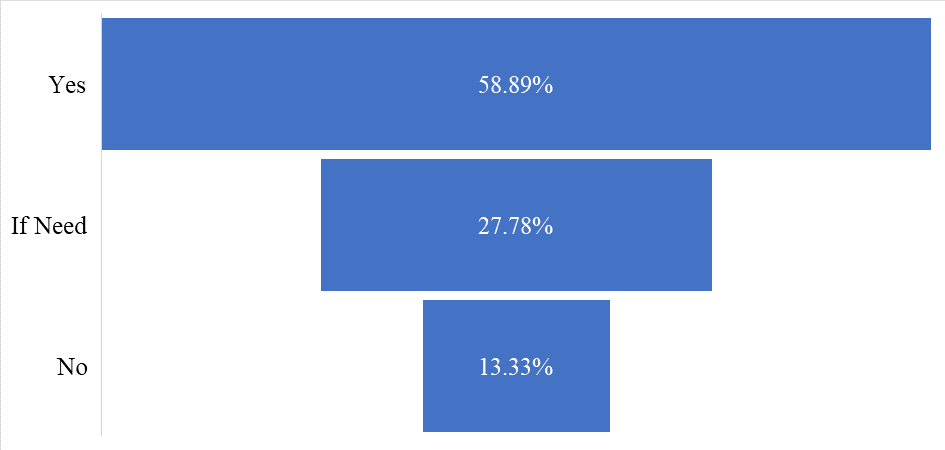

This funnel chart (Figure 10) illustrates the attitudes of mobile banking non-users regarding the adoption of MBS in the future. Among the 90 non-user respondents, 58.88% expressed an intention to adopt MBS in the future. Additionally, 27.77% indicated that they would adopt the service if necessary, while 13.33% stated that they do not plan to adopt mobile banking in the future.

5. Results and Discussion

Logistic regression analysis is used to identify the highly influential factors influencing MBS adoption. This model incorporates socio-economic, demographic, and high-dimensional explanatory variables. Results are compared with existing literature in the discussion section. A probable reason justifies the results of the study.

5.1 Results of the Study

Table 6 presents the logistic regression analysis, where the dependent variable (own mobile banking account) is a binary variable and several independent variables are considered. The age of the respondents (coefficient value -.1915) has shown a negative and statistically significant relationship with mobile banking service adoption. This means that (marginal value = -0.0073) for a one-year age increase, the possibility of mobile banking service decreased by 0.73 percent, and this result is statistically significant at a 1 percent level of significance. The result suggests that older people are less likely to adopt mobile banking. This means that the adoption rate of younger people is comparatively high. This is likely due to older respondents' lack of skills with technology or their unwillingness to adopt new digital platforms.

Table 6: Factors Influencing Adoption of Mobile Banking Service

| Variable(s) | Mobile Banking Usage | |||

|---|---|---|---|---|

| Unit of Measurement | Coefficient Value | Marginal Value | Standard Error | |

| Age | In year | -.1915*** | -0.0073*** | 0.0021 |

| Gender (Ref. Female) | ||||

| Male | Dummy | 2.899* | 0.1118* | 0.0623 |

| Educational Qualification | Years of Schooling | -.0604 | -0.0023 | 0.0063 |

| Marital Status (Ref. Unmarried) | ||||

| Married | Dummy | -1.914 | -0.0738 | 0.0622 |

| Religion (Ref. Muslim) | ||||

| Hindu | Dummy | -.8927 | -0.0344 | 0.0461 |

| Occupational Status (Ref. Others) | ||||

| Housewife | Dummy | -.8147 | -0.0314 | 0.0578 |

| Living Arrangement (Ref. Rent House) | ||||

| Own House | Dummy | -1.315 | -0.0507 | 0.0331 |

| Family Type (Ref. Nuclear) | ||||

| Joint | Dummy | -.3848 | -0.0148 | 0.0418 |

| Household Size | In numbers | -.2211 | -0.0085 | 0.0228 |

| Earning Member | In numbers | .0417 | 0.0016 | 0.0391 |

| Respondent Income | BDT/Month | -.00015 | -0.0000005 | 0.000000 |

| Respondent Expenditure | BDT/Month | .0012*** | 0.000048*** | 0.000014 |

| Respondents Savings | BDT/Month | .0066*** | 0.00025*** | 0.00005 |

| Ease of Use (EU) | Factor Score | 1.744** | 0.0672** | 0.0268 |

| Infrastructural Facilities (IF) | Factor Score | .5532 | 0.2134 | 0.0157 |

| Perceived Trust (PT) | Factor Score | 1.564** | 0.0603** | 0.0272 |

| Peer Influence (PI) | Factor Score | -.1131 | -0.0043 | 0.0260 |

| Perceived Risk (PR) | Factor Score | -1.502* | -0.0579* | 0.0296 |

| Robust standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1 | ||||

| Pseudo R2 = 0.7120 | ||||

Source: Field Survey, 2024

The gender of the respondents (coefficient value: 2.899) has shown a positive and statistically significant relationship with the adoption of mobile banking services. This means that (marginal value 0.1118) male respondents have 11 percent higher possibility than female respondents to adopt mobile banking service, and this result is statistically significant at the 10 percent level of significance. The reason is that men are more likely to engage in different kinds of jobs and income sources than women. As a result, males have better savings than that of females. Additionally, in our society, most families' financial transactions are conducted through male mobile banking accounts.

The respondents' expenditure (coefficient value .0012) has shown a positive and statistically significant relationship with mobile banking service adoption. This means that (marginal value 0.000048) for one taka expenditure increase, the possibility of mobile banking service adoption increased by 0.0048 percent, and this result is statistically significant at a 1 percent level of significance. The reason for this is that respondents with higher expenditures tend to have a more luxurious lifestyle. They use mobile banking accounts for various types of bill payments such as electricity, gas, water, and product bills. High-expenditure individuals have higher incomes. They are frequently engaged in large-scale financial transactions. Mobile banking service provides a convenient, fast, and efficient way to manage these activities.

The respondents' savings (with a coefficient value of 0.0066) have shown a positive and statistically significant relationship with the adoption of mobile banking services. This means that (marginal value 0.00025) for one taka additional savings, the possibility of mobile banking service adoption increased by 0.02 percent, and this result is statistically significant at a 1 percent level of significance. The results suggest that respondents with higher savings are more likely to adopt mobile banking. The reason for this is that the savings money they easily deposit into their mobile banking account and keep with them can be easily used when needed. Ease of use (with a coefficient value of 1.744) and mobile banking service adoption exhibit a positive and statistically significant relationship. It means that (marginal value 0.0672) if a one-point scale increases the ease of use, then the possibility of mobile banking service adoption increases by 6.72 percent. That result is statistically significant at a 5 percent level of significance. The Possible reasons for having a positive relationship are the benefits provided by mobile banking, such as user-friendly service, ease of use, low cost, and quick transaction service.

Perceived trust and mobile banking service adoption (coefficient value = 1.564) have a positive and statistically significant relationship. It means that (marginal value=0.0603) if a one-point scale increases the reliability in mobile banking service, then the possibility of mobile banking service adoption rises by 6.03 percent. That result is statistically significant at a 5 percent level of significance. Mobile banking has become reliable by providing reliable service, such as reliable customer service and customer agents. Perceived trust has significantly influenced respondents' willingness to adopt the mobile banking service. Perceived risk and mobile banking service adoption (coefficient value: -1.502) have a negative relationship, but this relationship is statistically significant. This means that (marginal value -0.0579) if a one-point scale increases the perceived risk, then mobile banking service adoption decreases by 5.28 percent. That result is statistically significant at a 10 percent level of significance. The perceived risks, such as hacking and compromising confidentiality, discourage people from adopting mobile banking services. The Pseudo R-squared value is 0.7120, indicating that the model explains 71.2% of the variance in the dependent variable.

5.2 Discussion of the Study

This study reveals that older individuals are less likely to utilize mobile banking, possibly because they find technology challenging or are hesitant to try digital services. Younger people adopt mobile banking more often. Studies of similar fields reveal that the younger generation prefers mobile banking more, as they are tech-savvy. Older people find MBS cumbersome because they are usually unfamiliar with digital gadgets (Lee et al., 2021; Suh and Han, 2002). Our outcomes indicate that males are more likely to adopt MBS compared to females, as males are often more engaged in financial transactions. Others opined that cultural norms and the way people handle financial decisions contribute to this situation. These mechanisms make it more difficult for females to use MBS (Islam, 2015; Suh and Han, 2002). Our results suggest that individuals who spend a significant amount of money are more likely to adopt MBS. It is easier for the person to make payments and manage plenty of transactions. Persons with a high tendency to save are more inclined to use MBS. They can make smooth savings and withdrawals of money using MBS. Other studies also support this scenario. Different research indicates that the more money transactions, the more frequent use of the MBS (Haider et al., 2018; Suh and Han, 2002). Our findings show that mobile banking is convenient and popular; people are eager to adopt it. Smooth and quick service motivates the adoption of MBS. Similarly, research in the related field reveals that ease of use is a key factor influencing mobile banking usage. This suggests that mobile banking apps are intuitive, user-friendly, and convenient. That is why people will be engaged more with it. Convenient operating procedure of MBS leads people to accept it (Akhter et al., 2020; Jadil et al., 2021; Khan et al., 2017). Our findings emphasize that if there is perceived trust in MBS, people are more inclined to use it. Reliable and flawless service, along with customer care, can boost this trust. Other studies also show that trust is a pivotal factor in adopting mobile finance services (MFS). If it is secure and reliable, people are willing to use this service. If mobile banking operators ensure the safety of the money and personal information, people feel much confident about MBS (Hossain and Hossain, 2015; Kabir, 2013).

This study shows that perceived risk in mobile banking service demotivates people from using it. Concerns about data breaches and hacking create distrust in mobile banking, discouraging its use despite its convenience. Another study yields similar results, highlighting risks associated with issues such as unauthorized access to personal information and the potential for hacking accounts. Concerns about privacy, such as third-party fraud of user data, can reduce trust in MBS, limiting their adoption (Islam, 2015; Haider et al., 2018).

6. Concluding Remarks

6.1 Findings of the Study

The most used MBS is Bkash. Mostly, people use MBS for bill payment. Adoption of MBS decreases with age. It means that younger people are more likely to adopt MBS. Males are more likely to adopt mobile banking services than females, as males are often closely associated with earning and financial issues. Respondents' expenditure has a positive relationship with MBS adoption because individuals with high expenditures are frequently engaged in large-scale financial transactions. Respondents' savings positively influence MBS adoption. MBS is more popular among respondents with higher savings because of its easy access. MBS offers a range of benefits, including user-friendly service, ease of use, low costs, and quick transaction processing. Perceived trust has a statistically significant positive relationship with MBS adoption. Mobile banking has become reliable by providing a reliable service. Perceived Risk has a statistically significant negative relationship with mobile banking service adoption. A possible reason for this is the perceived risk concerns leading to a lack of trust in the MBS. Infrastructural facilities have a positive relationship, while peer influence has a negative relationship. However, these cannot affect MBS significantly.

6.2 Recommendations and Policy Implications

Based on the results and findings, the authors found some drawbacks in the existing system. It is possible to improve the situation with some necessary steps. Those steps can enhance the usage of MBS and make people's lives easier. People will be able to use MBS according to their needs because of its versatile features.

6.3 Further Research Opportunities

Identifying further research options is a crucial aspect of concluding a research project, as it guides future scholars and researchers in building upon the current study. Here are some suggestions for further research options related to investigating the drivers of mobile banking services adoption in Khulna city.

6.4 Conclusion

The study identifies factors that influence the adoption of mobile banking in Khulna city. Key findings include the dominance of Bkash as a mobile banking tool and the primary use of mobile banking services for bill payments. Older individuals are less likely to adopt mobile banking services, whereas males tend to adopt them more readily. Socioeconomic factors, including higher savings and expenditures, significantly increase the likelihood of adopting mobile banking services. Primary factors, including ease of use and perceived trust, significantly improve the likelihood of adoption. Perceived risk has a negative impact, possibly due to the risk of account hacking. Peer influence and infrastructural facilities were not significant in influencing adoption. This study tried to find out the demographic factors, socio-economic factors, and some primary factors affecting mobile banking service adoption. Future studies can compare individuals who have adopted and those who have not, and conduct an analysis based on occupational status. The study findings suggest that promoting user trust, highlighting benefits, and simplifying processes can encourage more people to adopt mobile banking services.

References

Corresponding Author. E-mail: mehedi@econ.ku.ac.bd